Claim for Flood Damage for a property

The recent Australian big flood destroyed thousands of homes and property like cars and livestock. Had you prepared for the flood claim on your property yet? Now, it is time to study your policy closely on the clause on a flood damage claim. Call your agent for advice on how to claim flood damage on a property before it is too late. Natural disasters like floods or typhoons and tidal waves alway strike when you are off guard. Life is hard, isn’t? In reality, how to claim flood damage for a property? Surely, you purchased fire insurance on your house with flood extension, don’t you? Or else, you cannot claim flood damage on your property.

Claim for Flood Damage to Property

Has Mother Earth punished us for destroying the atmosphere? if Yes, we ought to face the music the consequences of global warming. Have we not learning a lesson yet?

The extraordinary continuous rainfall, in Penang and parts of Kedah on Nov 4 and 5 2017, The low-pressure area – the main cause of the flooding. It became a focal point for winds and a high level of moisture resulting in continuous heavy rain and strong winds.

Again, as can be seen, the recent 2019 Australian Bushfire, followed by the severe flood in 2020. Had our world leader taken a dramatic action to reduce global warming?

Flood Extension to House and Car in flood damage claim

Beyond the human tragedy, the widespread flood damage caused by the flood and heavy storm serves as an utmost urgent reminder to homeowners in Malaysia. Now, awake call to property owner to purchased flood extension coverage in order to mitigate future loss claims.

Your home is a sanctuary for your family. Do not save a penny resulting in pay up a fortune? Nevertheless, it is never too late to reexamine closely your home or fire insurance policy. Moreover, It does not cost you an arm and leg to have the flood extension coverage for your house and content with one easy plan.

How we could protect ourselves, rather than expecting the donor or government handout which is insufficient and takes an age to receive? Prevention may be a better cure, help ourselves. No point in crying the split milk later.!

Protect ourselves First

The following extension clauses highly recommend for the householder or house owner policy when entering a contract of insurance.

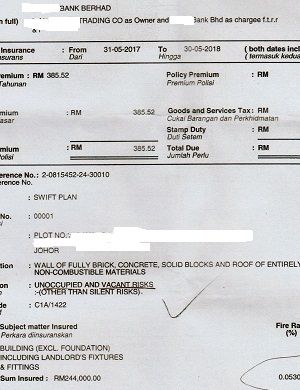

Flood extension with a rating of 0.086%, you would like to pay a further premium of $860.00 for the sum insured of $1 000 000.00. The insurer shall compensate for your flood damage to deal with structure or home contents.

Flood and damage claim on a property

The overflowing of water or deviate from its normal path. It is either due to prolonged hours of a heavy downpour. Besides, man makes a disaster like deforestation.

At the time, the Inundation from the general public mains supply. And also any flash flood water accumulation hails from outside the insured building.

Exclude the loss or damage caused by subsidence or landslip.

To complement the flood cover, the insured can also feature the subsidence

The movement of solid floor slabs below the external walls of the buildings damaged by the same cause and occur simultaneously

Likewise, it is the same for occurring or in consequence of coastal and river erosion. Demolish or alter structure or repair, defective design, and poor construct foundations.

No liability for the insurer in respect of every and each loss, 5% of the entire sum insured or $25 000.00 whichever is that the lower, after applying the law of averages.

How to delete the exclusion clause on the claim for flood damage on a property

Of course, you can delete it paying a further premium of 25% loading. Cover the outbuilding like the fence, gate, and walking path, dog kennel, and parking porch and swimming bath costs $500 000.00. Thus, you pay extra premium for the sum insured of $500 000.00 would be ($500 000 x 0.081% + 25% loading to delete the item 1) $506.25. Thus we derive the ultimate total premium for the extension peril would be ($810.00 + 506.25) = $1 316.25

Claim for flood damage by Falling Trees or Branches and Objects

The victims acknowledged not only the house submerged with water. But also the falling branches and tree fall the car parked within the car porch causing severe damage. Generally speaking, an insured claim flood damage to the house, but not on the car itself. Why not on both the properties, the insured got to ask their agent for their unprofessional work.

A wise move to cover the building and your car with such peril. By having said that, although it’s a painful lesson learned. Nevertheless, one can ensure this peril during subsequent renewal with a rating of 0.01%. Pay $100.00 for your property with a sum insured of $1 000 000.00

This Policy includes loss or damage to the property or to walls, gates, and fences directly damage due to falling trees or branches. The insured shall bear an excess of the $250.00 for every and any loss or damage. Don’t waste your precious time for the claim falls below $250.00. If the claim is $ 3 000.00, the insurer pays you $2 750.00 for the complete and final settlement of the claim. You bear your own cost of $250.00 for the claimed damage on your property.

Claim for flood damage on Removal of the debris (with the separated sum insured)

After the floodwater had receded, what a remain was a messy muddy floor. it’s an eyesore to ascertain floor carpet with mud, filthy muddy stagnant water. Life has got to continue. Has your ever think the cleaning process when hired workers to clean? What’s the value of this trying time? The cleaning company would demand an exorbitant fee for the laborious task which is in great demand. Does one check your policy for the removal of debris clause for the claim flood damage on your property?

The additional sum insured can incorporate forming a part of the sum insured with a separated sum. It all depends on the size of the building and the number of floors. ground. It can cost easily at $5 000.00 upward.

Prior approval from the Insurer

The insurer pays the insured for the prices and expenses necessarily incurred with the prior approval from insurance firm

(a) removal of debris

(b) dismantling and/or demolishing

(c) shoring or propping of the portion of property damaged or destroyed fire or by the other peril hereby insured against. (Items (b) and (c) above deemed to delete when neither Buildings nor machinery is insured).

No separated sum insured for the removal of debris

If the insured doesn’t feature a separated sum insured for the removal of debris. The insurer will bear 10% liability for the entire sum insured. The insured can claim up to $100,000 for cleaning up the mess out the sum insured of $1 000 000.00 provided flood extension clause printed within the policy.

Rent clause – to not overlook.

a) Applicable to owner non-occupier to the premise, if the building is unfit for occupation due fire or other insured peril, the owner for the rental loss shall not exceed the entire sum insured. Let say a monthly rental $2 000.00, loss of rental for six months can recover from an insurer of $12 000.00

b) Applicable to owner-occupier the premises, if the Penang flood destroyed the building, the insured got to find another alternative home for 1 year before a replacement home able to move in. The rental of an identical standard home cost $1000 per month, 12 months means the underwriter can pay $12 000.00 to the insured.

Claim for flood damage to a property

- Stay claim, the insured shall make a police report first.

Then, immediately inform the agent or insurer via telephone follow with an email to them. - Any unreasonable delays may prejudice your case. If the invisible agent isn’t available during the critical moment which quite a true fact in Malaysia, go straight to report back to the insurer directly.

- Don’t ever seek or consult over the cafe with friends or acquaintances for an opinion.

- Don’t waste your hard-earned money to hire rent a lawyer. As it may be a straightforward case, not a liability whereby you need to attend a court hearing.

- Liaise with the independent adjuster arrange by the insurer, allow them to have a radical inspection of the entire scene, invite their approval for any minor repair to mitigate further loss.

- Study closely the entire policy with the insurance broker for any exclusion of an excess clause. Any doubts please ask the insurer’s advice.

- Take a video clip of the damaged item for the adjuster inspection. Keep all the minor repair receipts. The video clip is of utmost importance for the claim dispute.

Summary on Claim for Flood Damage

- Duly completed sign original form with the repair invoice to the insurer and replica to the adjuster to expedite the claim.

- You make sure to have the acknowledgment of receiving the whole claim document by the insurance company. It is to avoid undue delay of not receiving your claim file.

- Don’t sign any counteroffer by the insurer unless you’re fully satisfied with the ultimate claim.

Lastly, You’ll read more on how to claim flood damage for a property.